Small Business Funding is participating in the PPP Program via our partner network. The PPP program is one of many small business funding options offered by Small Business Funding. Our suite of small business funding solutions include Working Capital Advances, Lines of Credit and SBA Loans. Learn about ALL of our funding options here.

To Apply for New PPP Funding or if you are applying a second time, click the link below.

Note – clicking this link will take you to our partner webpage to begin the application.

Program Details

About the PPP Program

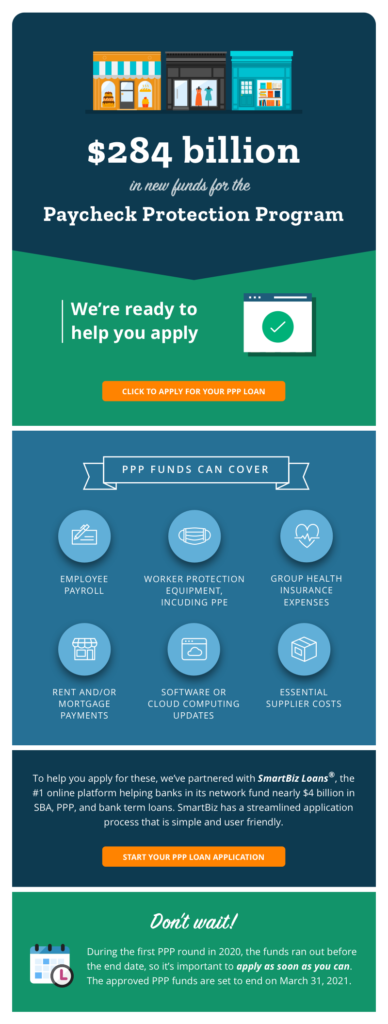

As part of a second round of relief for the COVID-19 pandemic, congress has passed the second round of the COVID stimulus package. The $900 billion COVID-19 relief package which is part of the Consolidated Appropriations Act, 2021. Included in this amount is $284 billion for a second round of what is known as the Paycheck Protection Program (PPP Program).

Businesses must be aware of some fundamental differences between this version of the PPP Program and the last version of this package.

The new relief package includes:

- New PPP loan funding

- The ability to obtain a second PPP Program loan for small businesses facing significant revenue declines in any 2020 quarter compared to the same quarter in 2019

- Clarifications providing for the deductibility of business expenses paid with forgiven PPP loans

- 15 billion for live venues, independent movie theaters and cultural institutions

- Loan eligibility for Section 501(c)(6) not-for-profit organizations for the first time

- $20 million for the Economic Injury Disaster Loan Program

The second round of the PPP Program has some key differences from the first round that are detailed below

Limited Eligibility for Second Round PPP Program Loans

The second round of PPP loans is available to not only first-time qualified borrowers but also to borrowers that previously received a PPP loan. PPP loans are limited to businesses that (i) employ no more than 300 employees or meet an alternative size standard; (ii) have used the entire amount of their first PPP loan or will use such amounts, and (iii) had gross receipts during Q1, Q2 or Q3 2020 that were at least 25 percent less than the gross receipts from the same quarter in 2019 (applicants may use Q4 2020 if they apply after January 1, 2021). If the business was not in operation for a portion of 2019, then the comparable quarters may be different.

Borrowers should be aware that the second round of PPP did not remove or change the necessity requirement. All borrowers must be able to certify that the “current economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant” as of the date on which the PPP loan application is submitted. More information can be obtained on the SBA website

Maximum Loan Amount

Borrowers have an option to calculate the maximum loan amount by multiplying the borrower’s average total monthly payroll in (a) the one-year period prior to the date on which the loan is made, or (b) calendar year 2019, by 2.5x. The maximum loan amount has been reduced from $10 million in the first round to $2 million. Similar to the first round, seasonal employers calculate their maximum loan amount differently.

Maximum Loan Amounts for the Hospitality Industry

Borrowers that have NAICS Code 72 (typically restaurants and hotels) are permitted to use a 3.5x multiplier of their average monthly payroll costs to calculate their maximum loan amount, subject to the $2 million cap.

Choose Your Own Covered Period

Originally the SBA provided that the covered period (the time in which a borrower must use the funds to qualify for forgiveness), would be an eight-week period beginning on the date the borrower received the loan proceeds. In subsequent amendments, the covered period was expanded to 24 weeks. In this latest round of PPP, borrowers are able to choose the length of their covered period so long as it is at least eight weeks and is not longer than 24 weeks. This subtle change will allow borrowers more control over how to handle potential reductions in workforce once the PPP funds are exhausted.

Use of PPP Funds

Congress expanded the types of expenses for which PPP loans can be used, which applies to existing PPP loans (except in the event forgiveness has already been obtained) and new loans. In addition to payroll, rent, covered mortgage interest and utilities, the PPP now allows proceeds to be used for:

- Covered Operations Expenditures: payments for business software or cloud computing service that facilitates business operations, product or service delivery, the processing, payment or tracking of payroll expenses, HR and billing functions, or account or tracking of supplies, inventory, records and expenses

- Covered Property Damage Costs: costs related to property damaged and vandalism or looting due to public disturbances that occurred during 2020 that was not covered by insurance or other compensation

- Covered Supplier Costs: expenditures to a supplier of goods that are essential to the operations of the entity at the time at which the expenditure was made and is made pursuant to a contract or order in effect at any time before the covered period or, with respect to perishable goods, in effect at any time during the covered period

- Covered Worker Protection Expenditures: operating or capital expenditures that allow a business to comply with requirements or guidance issued by the CDC, HHS, OSHA or any state or local government during the period beginning March 1, 2020 and ending on the date which the national emergency declared by the president expires related to the maintenance of standards for sanitation, social distancing or any other worker or customer safety requirement related to COVID-19. These expenses appear to include PPE, physical barriers that were put in place, expansion of indoor/outdoor space, ventilation or filtration systems and drive-through windows.

Tax Treatment

PPP loans will not be included as taxable income. Expenses paid with the proceeds of a PPP loan that is forgiven are now tax-deductible. This covers not only new loans but also existing and prior PPP loans, reversing previous guidance from the Treasury and IRS, which did not allow deductions on expenses paid for with PPP proceeds. In addition, any income tax basis increase that results from the borrower’s PPP Program loan will remain even if the PPP loan is forgiven.

EIDL Advances Do Not Reduce Forgiveness

Prior to the passage of the new Act, borrowers that received an EIDL Advance (advances between $1,000 and $10,000) had that amount subtracted from their total forgiveness, which, in effect, had the effect of repaying the EIDL Advance. The Act now provides that EIDL Advances will not reduce PPP loan forgiveness. The SBA has indicated that borrowers that already received forgiveness and had their EIDL Advance deducted from such forgiveness may be able to amend their forgiveness applications. Further guidance is expected to be issued.

Forgiveness Applications for Loans Under $150,000

Forgiveness application for loans under $150,000 will be simplified to a one-page certification that includes a description of the number of employees the eligible recipient was able to retain because of the loan, the estimated total amount of the loan spent on payroll costs and the total loan amount. Borrowers should be aware, however, that while the forgiveness application is simplified, all of the rules still apply. Rather than going through the process of showing how borrowers arrived at certain numbers, the simplified application merely asks borrowers to self-certify. Given the liability attached to making a false certification to the SBA, we advise all borrowers to use the long-form application to ensure that the certifications made on the simplified form are true and correct. Furthermore, all borrowers must retain all employment records relevant to the forgiveness application for a period of four years following the date of submission, and all other records relating to PPP and the forgiveness application for a period of three years following submission of the forgiveness application.

Eligibility for Section 501(c)(6) Not-for-Profit Organizations

For the first time, Section 501(c)(6) not-for-profit organizations will be eligible to apply for and receive PPP loans. These organizations generally consist of business leagues, chambers of commerce, real estate boards, boards of trade and professional football leagues, which are not organized for profit and no part of the net earnings of which inures to the benefit of any private shareholder or individual. These organizations are generally expected to be eligible so long as (i) they do not receive more than 15 percent of their receipts from lobbying activities, (ii) lobbying activities do not comprise more than 15 percent of the organization’s total activities, (iii) the cost of lobbying activities did not exceed $1 million during the tax year ending February 15, 2020, and (iv) the organization does not employ more than 300 employees.

For more information about this and other small business funding programs, contact us.