So you’re in need of a business loan – lucky for you there are a ton of options. You can always go to your local bank or one of the other big banks in your area. Or you can secure a loan through an online alternative lender.

You know what a bank is, but you may not know about alternative lending.

An alternative lender is a financial organization that provides funding options in the form of a Working Capital Advance, SBA Loan, Line of Credit, Term Loan or other solution to small businesses, outside of traditional bank lending and typically where the entire process is completed online.

But which option is best for the success of your business?

Here will we review the differences between a traditional bank versus an alternative lender, including which option would be best for your business.

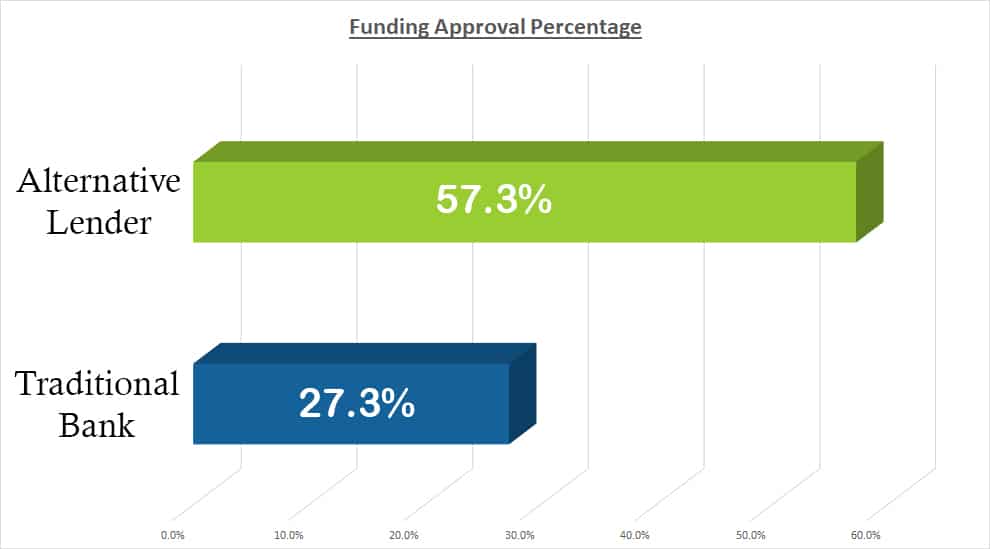

Ease of Funding

One of the primary reasons companies look into alternative lending is simply because the odds of them getting approved are greater.

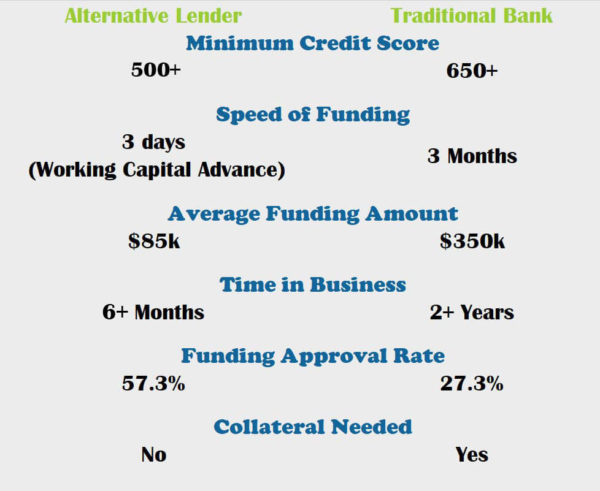

Below are the approval percentages for small business loan applicants at traditional banks versus alternative lenders (sources: Forbes).

Some of the reasons for the disparity are outlined below.

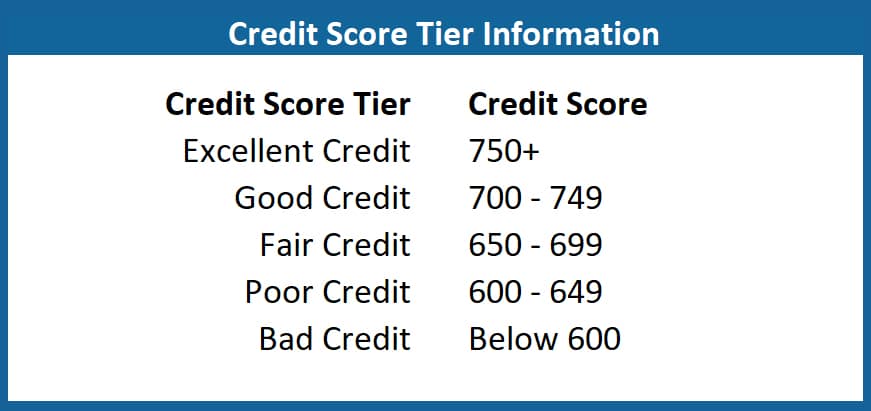

Credit Score

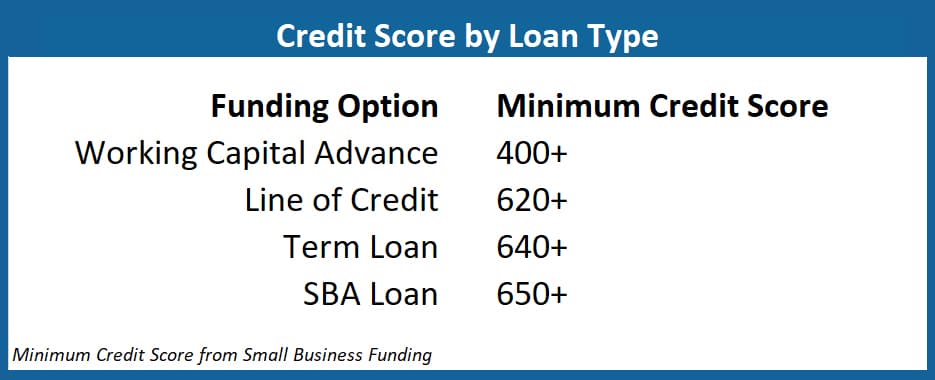

One of the biggest factors differentiating funding from a bank vs an alternative lender is your personal credit score, or FICO.

Every bank’s credit score requirements are different but on average a bank will require a credit score of 675 or higher. With lower credit scores resulting in a higher interest rate.

By contrast, many alternative lenders carry a minimum credit score of 500.

Most alternative lenders are willing to look past a low credit score because they place more emphasis on the health of your business. Specifically, alternative lenders want to see if the cash flow can actually support repayment in the short term.

Where your credit score will come into play is in determining what funding options your business may qualify for.

Age of Business

According to the Small Business Administration, about 20% of businesses fail the first year. In order to minimize their risk, lending organizations will require a minimum amount of time in business. However, age of business for banks and alternative lenders are based on how long you’ve had a business bank account, not necessarily how long you’ve had your business.

For example, here at Small Business Funding we want to see that you’ve been in business at least 3 months, and that the business generates gross monthly revenue of at least $8k in order to potentially qualify for business funding.

Keep in mind this is the minimum, and some of our funding options will have slightly higher requirements

Most traditional banks will require a minimum age of business of 2 years.

Collateral

Collateral is the securing of assets such has real estate, equipment, automobiles, etc. that a lender can reclaim and sell should you not satisfy your debt.

Depending on the business loan type, traditional banks may require security from default in the form of collateral. They will use a loan-to-value ratio to determine the amount you are able to borrow. This value is typically 60%-80% of the assets appraised value.

Alternative lenders do not always require collateral.

So why do banks require collateral, but alternative lenders do not?

Simple, banks are looking to make a profit from every loan. If there’s a chance you may default, they want to ensure they can secure some assets to sell.

Alternative lenders are also in business to make money but view small businesses as the backbone of our economy.

Small Business Funding, for example, views our small business clients as a partner. As such, when you’re successful, we’ll be successful. It’s in our best interest to ensure you have the funding needed to grow your business.

Some of our funding options, such as a Working Capital Advance, actually allow for adjustments in repayment terms depending on the most recent month’s revenue.

Average Funding

The average funded amount to a small business from an alternative lender is $85,000, but the range varies from as little as $5,000 to $1 million.

Conversely, the average funding from a bank is $350,000. Depending on the bank, they may have a minimum loan requirement of $50,000 – $100,000 but will fund as high as a several million dollars.

Interest Rates

Not all funding options offered by alternative lenders carry an interest rate, and they may have repayment terms that are based on your company’s revenue. Those funding products that do have an interest rate will tend to be higher than a traditional bank.

Traditional banks can keep their interest rates low because they minimize their risk by funding less risky businesses, those that have a strong personal credit score and history of making payments on time.

Time Involved

The initial process with a bank can take as much as 60 – 90 days just for an approval.

Why so long?

Banks have a system where multiple officials and employees review your application. In addition to this process, there is a lot of paperwork which needs to be completed and reviewed.

In most cases, an alternative lender will have an answer on your funding status within 24 hours of submitting a completed application, and you can potentially receive that funding within 72 hours (sooner in some cases). This will depend on the funding option you’re eligible for, and whether or not you are approved.

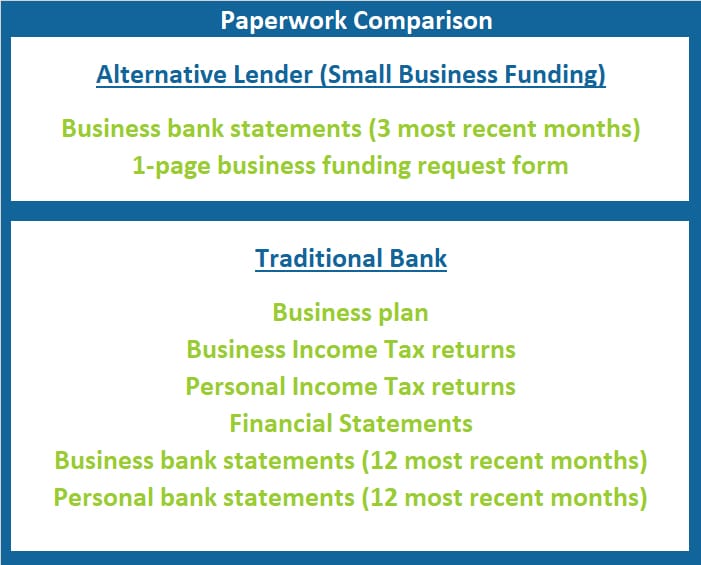

Paperwork

Traditional banks require significantly more upfront paperwork to complete an application than an alternative lender.

Below is a comparison.

What’s Best For You?

Both types of lenders have their pros and cons. Ultimately the lender you go with should depend on several factors including:

1 – your personal credit score

2 – how quickly you need funding

3 – how much money you need

4 – how long you’ve been in business

5 – your level of comfort

6 – length of loan

Initially, your options might depending more on your personal credit score. If your score isn’t strong, your best option (and possibly your only) is with an alternative lender. With a low credit score, your total repayment amount will be higher, and the payback period will be shorter.

In this case it could make sense to obtain a loan/advance with an alternative lender. Use this option while you work to improve your credit score, as a higher credit score could open up more funding options in the future. At the very least you are establishing a history of on-time payments with the alternative lender. This could make getting a second loan/advance with that lender easier.

If you have a strong credit score, you have more options. You will most likely be able to get the best rate and terms with a bank. But if you default, you run the risk of losing the assets you put up as collateral. With an alternative lender, we will work with you if you’re having trouble making payments. Again, your success is our success.

Beware of shopping for the best rate and terms with multiple banks. Each bank will likely run your credit report every time. Multiple credit pulls in a short time frame will start to lower your score.

Small Business Funding has a network of lenders it works with, so you don’t have to shop. We will work with our partners to find you the best option based on your business needs.

Let us know your thoughts on FACEBOOK and TWITTER

Click icons below to share.