If you own a small business or startup, it’s easy to use your personal credit card for some, maybe even all, of your business expenses. It’s convenient. You already have a credit card and it’s always on you.

You may even feel it’s your only option in order to maintain your business.

In fact, many entrepreneurs started their company by putting their business expenses on their personal credit cards. And they’ve just maintained this way of doing business.

Advantages…

1 – Rewards, Rewards, Rewards

The main benefit most business owners will state is:

“I get rewards for every dollar I spend”

If you spend enough each month, you start accumulating points for travel, hotels, and cash back.

2 – Consumer Protections

In 2009, the U.S. Congress passed the Credit Card Accountability, Responsibility, and Disclosure Act (also known as CARD Act of 2009). This bill was designed to protect consumers from unfair practices by the credit card companies.

The main benefits of this act is it prevents credit card providers from charging high fees and/or increasing interest rates. So other specifics of the bill is credit card providers must:

- Notify you if you’re about to exceed your credit limit. There is still a fee for going over your limit, but you will know be given the option to exceed your limit

- Statements must be mailed at least 21 days before the due date.

- The disclosures are more transparent.

Disadvantages…

1 – Hurt Your Personal Credit Score

Putting all or some of your business expenses may ultimately end up hurting your personal credit score.

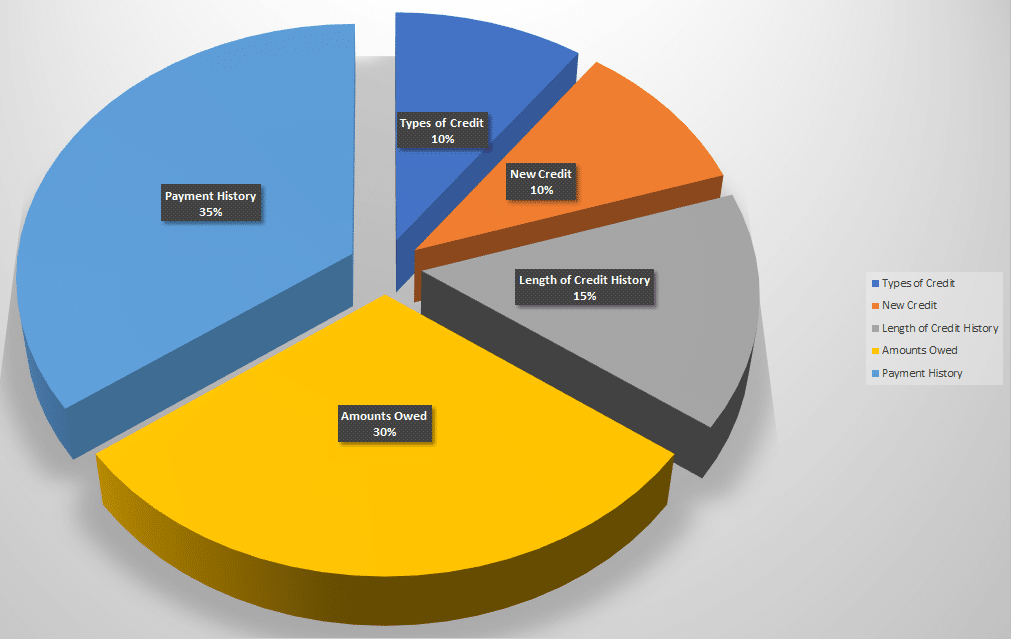

Obviously paying late, defaulting on your credit card will damage your score. These are the most important factors in determining your credit score. As they have a 35% influence on your score.

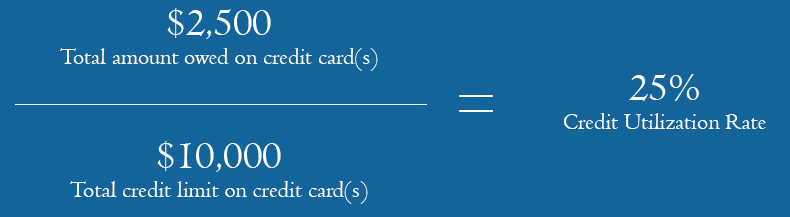

But one area business owners are typically not aware of that can have a major impact on your credit score is your credit to debt ratio, also known as credit utilization.

This just happens to be the second most important part in determining your credit score. Exceeding a 30% credit utilization potentially could lower your credit score.

Determining your credit utilization is simple, just divide your total balance by your credit limit.

Keep in mind that your credit score is calculated based on the most recent information posted on your credit report. So even though at the end of the month you may pay down your bill to be below 30% threshold, this will not matter if your credit report is run in the middle of a billing cycle.

Here are the factors that go into determining your credit score:

2 – Spending Limit

As your business grows, so will your expenses. Your credit card limit may range anywhere between $5,000 and $15,000. These factors depend on your credit score, income, and debt.

If you have a credit limit of $15,000, then really you can comfortably put $5,000 in business and personal expenses a month without exceeding the 30% credit utilization.

Eventually this just won’t be enough to run your business.

3 – Won’t Build Business Credit

Your personal credit activity is reported to the consumer credit bureaus. Whereas your business activity is reported to the business credit bureaus.

Similar to your personal credit score, a business credit score is used by most business lenders to predict your company’s ability to pay your bills in a timely manner.

Eventually you’re going to want to improve this score. This will allow lenders to take a closer look at your business performance and ability to pay bills when determining the likelihood of providing your company with a loan.

Other companies you want to do business with may look at your business credit score. If this score is low, they may not sell you products or service necessary for the success of your business.

4 – IRS Audit

Mixing your business and personal expenses may draw the attention of the IRS. If your business gets audited, you will need to prove to the satisfaction of the IRS which expenses where business vs personal.

Failure to do so could have you facing serious penalties.

5 – It Can “Pierce The Corporate Veil”

What does “Piercing The Corporate Veil” mean?

It is common to structure your business as a LLC (Limited Liability Corporation), S-Corporation, or C-Corporation. One of the rules under these structures is to keep your business and personal finances separate.

Usually a corporation is treated as a separate entity that is solely responsible for its debts and credits. However, when you commingle your personal and business expenses, such as on a credit card and fail to keep proper records, the courts could rule that you are a single entity.

In the case of a business liability, your personal assets could be at stack.

Don’t lose your business legal protection, make sure your business and personal expenses are separate.

Summary…

The dangers of using your personal credit card for business expenses far outweigh the advantages. The risks are just too great for your business and personal assets.

By not putting business expenses on your credit card, you may actually improve your personal credit score by lowering your credit utilization. This can help you get a business loan with a better rate in the future.

If you need funding now, in order to cover those expenses your were putting on your credit card, there are options. You can look into a business credit card and/or a working capital advance.